LIFE INSURANCE

Life insurance is a mechanism to guard against life’s uncertainties and helps surviving family members maintain their lifestyle. In, addition life insurance does something that no other financial product can do-it enables families to pass on more assets from one generation to the next. According to David Hughes, insurance should form the bedrock of any financial plan.

This means ensuring some protection is in place to pay out a lump sum in the event of death or disability. You must remember that “One should never be worth more dead than alive.”

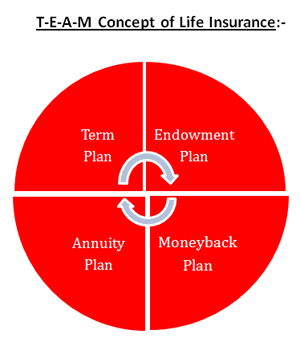

Life Insurance Plans:

Traditionally, four basic types of life Insurance plans are on offer in the market.

Term Plan – Life is Precious:

It provides more risk cover for a small investments and pays a lump sum on the death of the insured. The premium charged in term insurance does not have any saving element and hence the insured does not receive any maturity benefit. Financial planners can advise clients in younger age groups with growing responsibilites, low affordability and high insurability to go for the term plan.

Endowment Plan:

It is a traditional insurance plan that provides insurance cover as well as a return on maturity. It provides a safe/guaranteed return.

Money-back Plan:

Money-back plans and child plans are variants of endowment plans. Like, endowment plans, money back plans can be aligned to intemediate goals such as accumulating margin money for seeking home loan, to pay off tution fee or to buy/replace consumer durables etc.

Annuity Plan:- (Pension Relives Tension)

One cannot lose sight that old age is certainty of life. Pension is an essential tool and helps maintain a desired standard of living through the sunset years. Annuities are a financial planning tool that can help people save ant then provide them with variety of pay out options, including a secure and steady stream of income.